FIFO vs LIFO: Inventory Valuation Guide

Compare FIFO and LIFO inventory methods, how they affect cost and cash flow, and why accurate stock movement tracking matters.

Take 100 units of the same product, bought at different prices over three months. Sell 60 of them. The actual cash spent doesn't change — but depending on which accounting method you use, your reported profit, tax bill, and balance sheet can look dramatically different.

Choosing between FIFO and LIFO isn't just an accounting formality. It flows through your income statement, your taxes, and how your books look to a lender or investor.

FIFO vs LIFO

Image: Advance Storage Products

Image: Advance Storage Products

Neither method requires your warehouse to physically operate a certain way — it's a cost accounting assumption, not a warehouse rule.

FIFO (First In, First Out) | LIFO (Last In, First Out) | |

|---|---|---|

Core assumption | Oldest inventory sold first | Newest inventory sold first |

COGS in inflation | Lower | Higher |

Ending inventory value | Higher | Lower |

Reported profit | Higher | Lower |

Tax liability (inflation) | Higher | Lower |

Allowed under IFRS | Yes | No |

Allowed under US GAAP | Yes | Yes |

Best fit | Perishables, global businesses | US-only, tax deferral in inflation |

Critical: LIFO is not permitted under IFRS. If your business operates internationally, the decision is already made — FIFO is your only option.

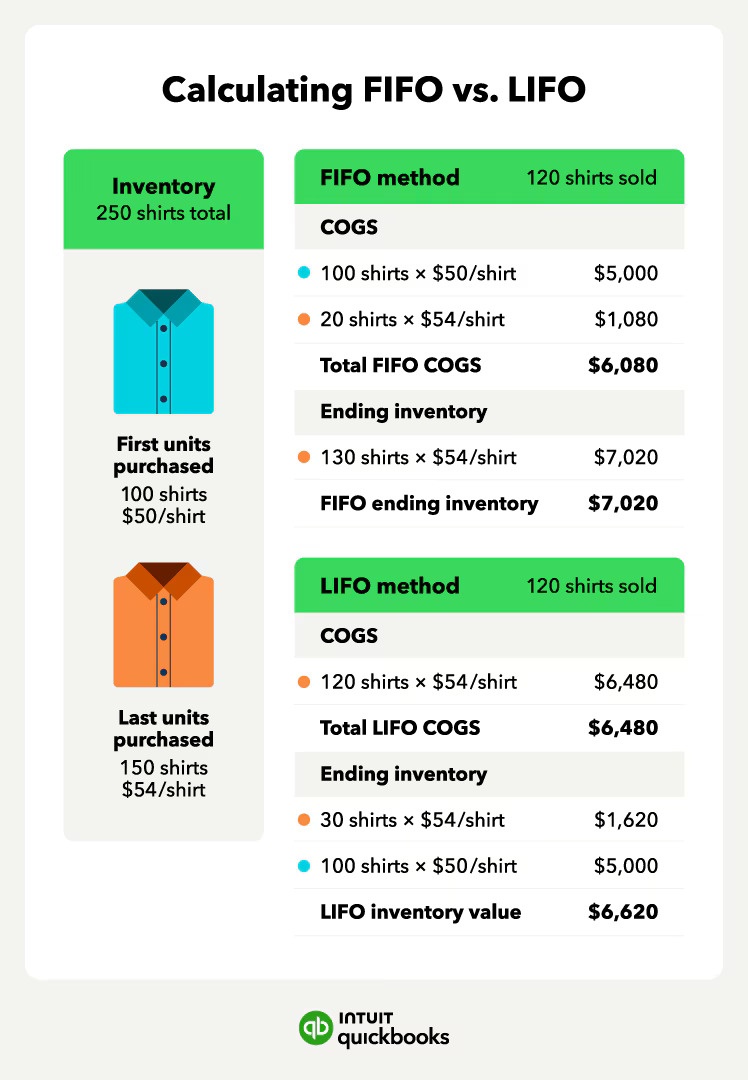

Image: QuickBooks - Intuit

Image: QuickBooks - Intuit

Difference Between FIFO and LIFO: Quick Answer

The difference between FIFO and LIFO is which inventory cost layer is treated as sold first. FIFO assumes the oldest inventory costs are sold first. LIFO assumes the newest inventory costs are sold first.

| Method | Cost assumption | Usually shows during rising costs | Best fit |

|---|---|---|---|

| FIFO | First purchased items are expensed first | Lower COGS, higher profit, higher ending inventory | Perishable goods, international reporting, simpler inventory valuation |

| LIFO | Most recently purchased items are expensed first | Higher COGS, lower taxable income, lower ending inventory | US businesses evaluating tax deferral during inflation |

FIFO and LIFO are accounting methods, not necessarily physical warehouse rules. A warehouse may physically ship older stock first while the accounting method still determines how costs are assigned in the books.

FIFO vs LIFO: Same Inventory, Different Numbers

Scenario: A distributor buys 300 units across three months, then sells 200.

Purchase | Units | Unit Cost | Total |

|---|---|---|---|

January | 100 | $10.00 | $1,000 |

February | 100 | $12.00 | $1,200 |

March | 100 | $14.00 | $1,400 |

Total | 300 | — | $3,600 |

Under FIFO (oldest sold first — Jan + Feb batches):

COGS = $2,200 | Ending inventory = $1,400 | Gross profit = $1,400

Under LIFO (newest sold first — Mar + Feb batches):

COGS = $2,600 | Ending inventory = $1,000 | Gross profit = $1,000

Same inventory. Same revenue. FIFO reports $400 more in gross profit and $400 more in inventory value — but LIFO produces $400 less in taxable income. At $5M in annual COGS, that gap can represent tens of thousands of dollars in tax liability.

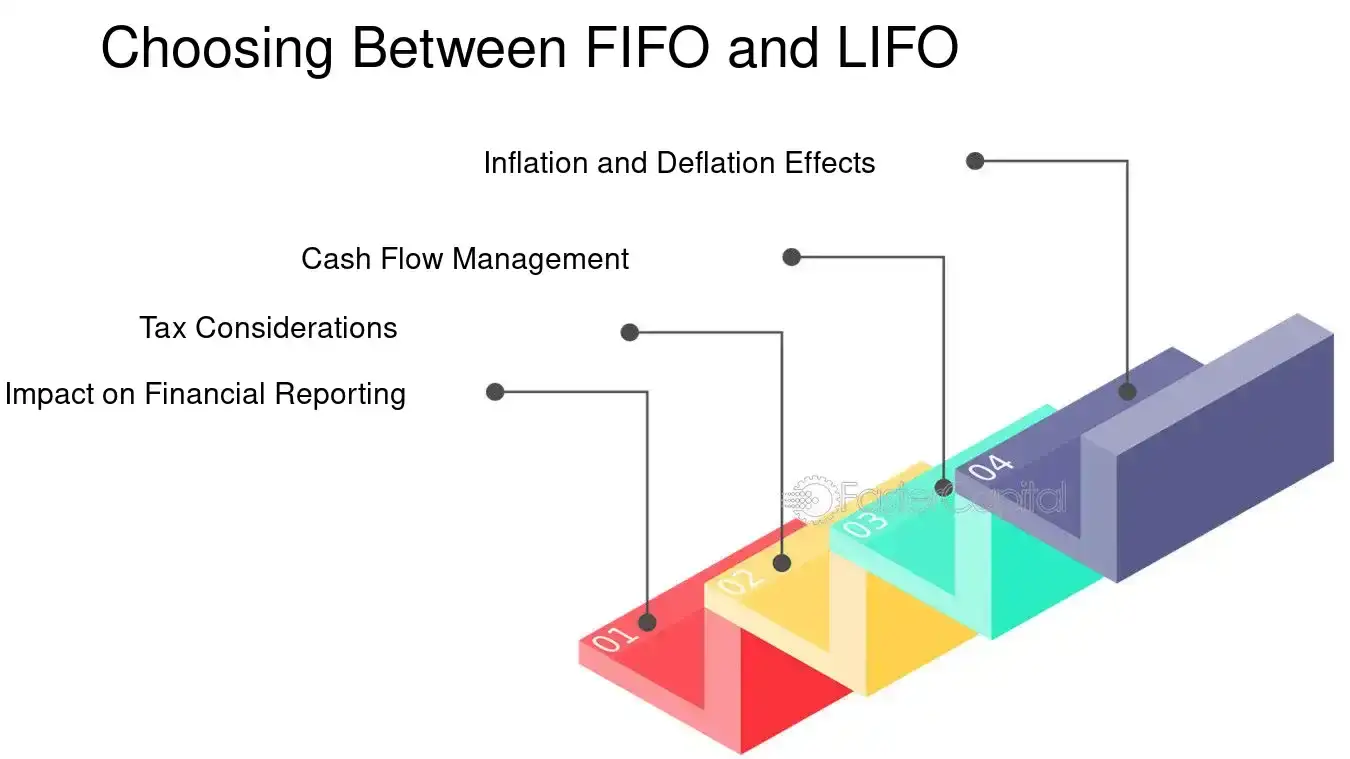

How FIFO and LIFO Affect Cash Flow, Taxes, and Inventory Value

Image: FasterCapital

Image: FasterCapital

Cash flow: LIFO's lower reported income means lower tax payments now — keeping more cash in the business short-term. FIFO does the opposite: higher reported profit, higher taxes, less available cash despite identical operations.

Tax strategy:

US-based businesses under GAAP can use LIFO as a tax deferral tool in inflationary periods. The benefit is real, but it's deferral — not elimination.

The IRS LIFO conformity rule means you can't use LIFO for taxes and FIFO for investor statements. One method, applied consistently.

Balance sheet: FIFO values ending inventory at recent purchase prices — closer to replacement cost, better for borrowing. LIFO's understated inventory value can reduce credit line capacity.

💡 Watch for LIFO liquidation: if you sell down inventory faster than you replenish it, older low-cost layers get expensed — inflating profits and triggering an unexpected tax bill.

How to Choose Between FIFO vs LIFO: A Decision Framework

No single right answer — work through these conditions for your specific situation.

→ Perishables or time-sensitive products: FIFO. Selling oldest stock first is physically necessary, not just an accounting preference. Food, pharma, seasonal fashion, and electronics all fit here.

→ IFRS reporting or international expansion planned: FIFO. LIFO is prohibited under IAS 2. Switching methods later requires restating historical financials — expensive and disruptive.

→ US-based, rising input costs, want to reduce current-year taxes: LIFO is worth evaluating. Run the numbers with your accountant first — electing LIFO requires IRS Form 970, and switching back is restricted.

→ Stable product costs: The FIFO vs LIFO gap shrinks when prices don't move much. FIFO's simplicity and IFRS compatibility make it the default.

→ Balance sheet used for lending or investor reporting: FIFO. Higher inventory values and reported profits matter for credit applications and valuation multiples.

These aren't hard rules. A commodity distributor with no international exposure might legitimately prefer LIFO for tax efficiency.

A fashion retailer with write-off risk will almost always prefer FIFO to avoid dead stock piling up at undervalued costs.

When in doubt, run the numbers both ways on your actual purchase history before committing.

Whichever Method You Choose, Tracking Is What Makes It Work

Image: CIN7

Image: CIN7

FIFO and LIFO only produce accurate results if your underlying inventory data is reliable. FIFO cost layers need to be tracked in sequence. LIFO requires knowing which inventory was most recently acquired. Both require purchase price history that doesn't disappear when someone reformats a spreadsheet.

Accurate inventory valuation starts with accurate inventory records. If your current tracking relies on spreadsheets and manual entry, StackCube gives small distributors a structured system for inventory and purchase order tracking from day one.

Explore the fundamentals:

What is inventory management? — Core concepts and system types

Inventory management best practices — How to structure tracking that holds up

How to choose inventory management software — What to evaluate before you buy